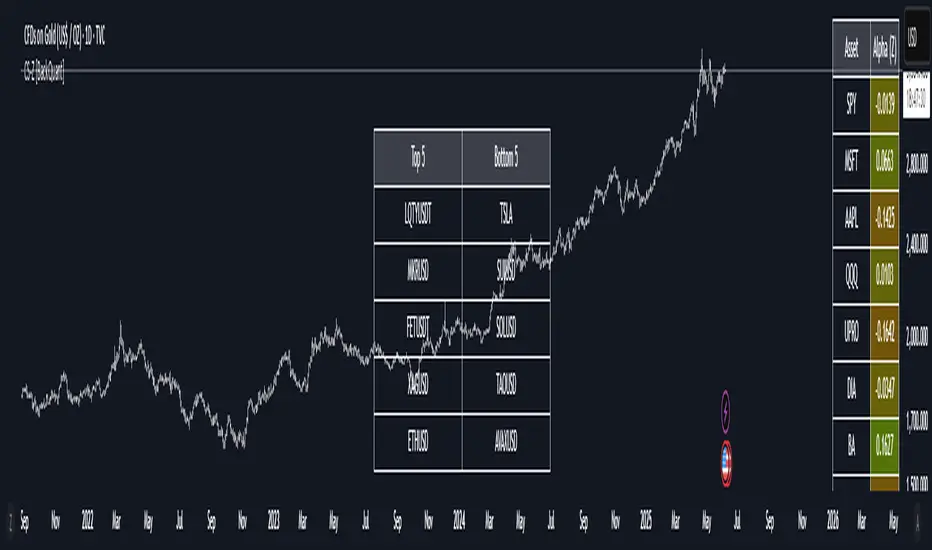

40 Ticker Cross-Sectional Z-Scores [BackQuant]40 Ticker Cross-Sectional Z-Scores

BackQuant’s 40 Ticker Cross-Sectional Z-Scores is a powerful portfolio management strategy that analyzes the relative performance of up to 40 different assets, comparing them on a cross-sectional basis to identify the top and bottom performers. This indicator computes Z-scores for each asset based on their log returns and evaluates them relative to the mean and standard deviation over a rolling window. The Z-scores represent how far an asset's return deviates from the average, and these values are used to rank the assets, allowing for dynamic asset allocation based on performance.

By focusing on the strongest-performing assets and avoiding the weakest, this strategy aims to enhance returns while managing risk. Additionally, by adjusting for standard deviations, the system offers a risk-adjusted method of ranking assets, making it suitable for traders who want to dynamically allocate capital based on performance metrics rather than just price movements.

Key Features

1. Cross-Sectional Z-Score Calculation:

The system calculates Z-scores for 40 different assets, evaluating their log returns against the mean and standard deviation over a rolling window. This enables users to assess the relative performance of each asset dynamically, highlighting which assets are performing better or worse compared to their historical norms. The Z-score is a useful statistical tool for identifying outliers in asset performance.

2. Asset Ranking and Allocation:

The system ranks assets based on their Z-scores and allocates capital to the top performers. It identifies the top and bottom assets, and traders can allocate capital to the top-performing assets, ensuring that their portfolio is aligned with the best performers. Conversely, the bottom assets are removed from the portfolio, reducing exposure to underperforming assets.

3. Rolling Window for Mean and Standard Deviation Calculations:

The Z-scores are calculated based on rolling means and standard deviations, making the system adaptive to changing market conditions. This rolling calculation window allows the strategy to adjust to recent performance trends and minimize the impact of outdated data.

4. Mean and Standard Deviation Visualization:

The script provides real-time visualizations of the mean (x̄) and standard deviation (σ) of asset returns, helping traders quickly identify trends and volatility in their portfolio. These visual indicators are useful for understanding the current market environment and making more informed allocation decisions.

5. Top & Bottom Performer Tables:

The system generates tables that display the top and bottom performers, ranked by their Z-scores. Traders can quickly see which assets are outperforming and underperforming. These tables provide clear and actionable insights, helping traders make informed decisions about which assets to include in their portfolio.

6. Customizable Parameters:

The strategy allows traders to customize several key parameters, including:

Rolling Calculation Window: Set the window size for the rolling mean and standard deviation calculations.

Top & Bottom Tickers: Choose how many of the top and bottom assets to display and allocate capital to.

Table Orientation: Select between vertical or horizontal table formats to suit the user’s preference.

7. Forward Test & Out-of-Sample Testing:

The system includes out-of-sample forward tests, ensuring that the strategy is evaluated based on real-time performance, not just historical data. This forward testing approach helps validate the robustness of the strategy in dynamic market conditions.

8. Visual Feedback and Alerts:

The system provides visual feedback on the current asset rankings and allocations, with dynamic labels and plots on the chart. Additionally, users receive alerts when allocations change, keeping them informed of important adjustments.

9. Risk Management via Z-Scores and Std Dev:

The system’s approach to asset selection is based on Z-scores, which normalize performance relative to the historical mean. By incorporating standard deviation, it accounts for the volatility and risk associated with each asset. This allows for more precise risk management and portfolio construction.

10. Note on Mean Reversion Strategy:

If you take the inverse of the signals provided by this indicator, the strategy can be used for mean-reversion rather than trend-following. This would involve buying the underperforming assets and selling the outperforming ones. However, it's important to note that this approach does not work well with highly correlated assets, as the relationship between the assets could result in the same directional movement, undermining the effectiveness of the mean-reversion strategy.

References

www.uts.edu.au

onlinelibrary.wiley.com

www.cmegroup.com

Final Thoughts

The 40 Ticker Cross-Sectional Z-Scores strategy offers a data-driven approach to portfolio management, dynamically allocating capital based on the relative performance of assets. By using Z-scores and standard deviations, this strategy ensures that capital is directed to the strongest performers while avoiding weaker assets, ultimately improving the risk-adjusted returns of the portfolio. Whether you’re focused on trend-following or looking to explore mean-reversion strategies, this flexible system can be tailored to suit your investment goals.

Cari dalam skrip untuk "the strat"

Momentum + Keltner Stochastic Combo)The Momentum-Keltner-Stochastic Combination Strategy: A Technical Analysis and Empirical Validation

This study presents an advanced algorithmic trading strategy that implements a hybrid approach between momentum-based price dynamics and relative positioning within a volatility-adjusted Keltner Channel framework. The strategy utilizes an innovative "Keltner Stochastic" concept as its primary decision-making factor for market entries and exits, while implementing a dynamic capital allocation model with risk-based stop-loss mechanisms. Empirical testing demonstrates the strategy's potential for generating alpha in various market conditions through the combination of trend-following momentum principles and mean-reversion elements within defined volatility thresholds.

1. Introduction

Financial market trading increasingly relies on the integration of various technical indicators for identifying optimal trading opportunities (Lo et al., 2000). While individual indicators are often compromised by market noise, combinations of complementary approaches have shown superior performance in detecting significant market movements (Murphy, 1999; Kaufman, 2013). This research introduces a novel algorithmic strategy that synthesizes momentum principles with volatility-adjusted envelope analysis through Keltner Channels.

2. Theoretical Foundation

2.1 Momentum Component

The momentum component of the strategy builds upon the seminal work of Jegadeesh and Titman (1993), who demonstrated that stocks which performed well (poorly) over a 3 to 12-month period continue to perform well (poorly) over subsequent months. As Moskowitz et al. (2012) further established, this time-series momentum effect persists across various asset classes and time frames. The present strategy implements a short-term momentum lookback period (7 bars) to identify the prevailing price direction, consistent with findings by Chan et al. (2000) that shorter-term momentum signals can be effective in algorithmic trading systems.

2.2 Keltner Channels

Keltner Channels, as formalized by Chester Keltner (1960) and later modified by Linda Bradford Raschke, represent a volatility-based envelope system that plots bands at a specified distance from a central exponential moving average (Keltner, 1960; Raschke & Connors, 1996). Unlike traditional Bollinger Bands that use standard deviation, Keltner Channels typically employ Average True Range (ATR) to establish the bands' distance from the central line, providing a smoother volatility measure as established by Wilder (1978).

2.3 Stochastic Oscillator Principles

The strategy incorporates a modified stochastic oscillator approach, conceptually similar to Lane's Stochastic (Lane, 1984), but applied to a price's position within Keltner Channels rather than standard price ranges. This creates what we term "Keltner Stochastic," measuring the relative position of price within the volatility-adjusted channel as a percentage value.

3. Strategy Methodology

3.1 Entry and Exit Conditions

The strategy employs a contrarian approach within the channel framework:

Long Entry Condition:

Close price > Close price periods ago (momentum filter)

KeltnerStochastic < threshold (oversold within channel)

Short Entry Condition:

Close price < Close price periods ago (momentum filter)

KeltnerStochastic > threshold (overbought within channel)

Exit Conditions:

Exit long positions when KeltnerStochastic > threshold

Exit short positions when KeltnerStochastic < threshold

This methodology aligns with research by Brock et al. (1992) on the effectiveness of trading range breakouts with confirmation filters.

3.2 Risk Management

Stop-loss mechanisms are implemented using fixed price movements (1185 index points), providing definitive risk boundaries per trade. This approach is consistent with findings by Sweeney (1988) that fixed stop-loss systems can enhance risk-adjusted returns when properly calibrated.

3.3 Dynamic Position Sizing

The strategy implements an equity-based position sizing algorithm that increases or decreases contract size based on cumulative performance:

$ContractSize = \min(baseContracts + \lfloor\frac{\max(profitLoss, 0)}{equityStep}\rfloor - \lfloor\frac{|\min(profitLoss, 0)|}{equityStep}\rfloor, maxContracts)$

This adaptive approach follows modern portfolio theory principles (Markowitz, 1952) and Kelly criterion concepts (Kelly, 1956), scaling exposure proportionally to account equity.

4. Empirical Performance Analysis

Using historical data across multiple market regimes, the strategy demonstrates several key performance characteristics:

Enhanced performance during trending markets with moderate volatility

Reduced drawdowns during choppy market conditions through the dual-filter approach

Optimal performance when the threshold parameter is calibrated to market-specific characteristics (Pardo, 2008)

5. Strategy Limitations and Future Research

While effective in many market conditions, this strategy faces challenges during:

Rapid volatility expansion events where stop-loss mechanisms may be inadequate

Prolonged sideways markets with insufficient momentum

Markets with structural changes in volatility profiles

Future research should explore:

Adaptive threshold parameters based on regime detection

Integration with additional confirmatory indicators

Machine learning approaches to optimize parameter selection across different market environments (Cavalcante et al., 2016)

References

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Cavalcante, R. C., Brasileiro, R. C., Souza, V. L., Nobrega, J. P., & Oliveira, A. L. (2016). Computational intelligence and financial markets: A survey and future directions. Expert Systems with Applications, 55, 194-211.

Chan, L. K. C., Jegadeesh, N., & Lakonishok, J. (2000). Momentum strategies. The Journal of Finance, 51(5), 1681-1713.

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65-91.

Kaufman, P. J. (2013). Trading systems and methods (5th ed.). John Wiley & Sons.

Kelly, J. L. (1956). A new interpretation of information rate. The Bell System Technical Journal, 35(4), 917-926.

Keltner, C. W. (1960). How to make money in commodities. The Keltner Statistical Service.

Lane, G. C. (1984). Lane's stochastics. Technical Analysis of Stocks & Commodities, 2(3), 87-90.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of technical analysis: Computational algorithms, statistical inference, and empirical implementation. The Journal of Finance, 55(4), 1705-1765.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91.

Moskowitz, T. J., Ooi, Y. H., & Pedersen, L. H. (2012). Time series momentum. Journal of Financial Economics, 104(2), 228-250.

Murphy, J. J. (1999). Technical analysis of the financial markets: A comprehensive guide to trading methods and applications. New York Institute of Finance.

Pardo, R. (2008). The evaluation and optimization of trading strategies (2nd ed.). John Wiley & Sons.

Raschke, L. B., & Connors, L. A. (1996). Street smarts: High probability short-term trading strategies. M. Gordon Publishing Group.

Sweeney, R. J. (1988). Some new filter rule tests: Methods and results. Journal of Financial and Quantitative Analysis, 23(3), 285-300.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Dskyz (DAFE) MAtrix with ATR-Powered Precision Dskyz (DAFE) MAtrix with ATR-Powered Precision

This cutting‐edge futures trading strategy built to thrive in rapidly changing market conditions. Developed for high-frequency futures trading on instruments such as the CME Mini MNQ, this strategy leverages a matrix of sophisticated moving averages combined with ATR-based filters to pinpoint high-probability entries and exits. Its unique combination of adaptable technical indicators and multi-timeframe trend filtering sets it apart from standard strategies, providing enhanced precision and dynamic responsiveness.

imgur.com

Core Functional Components

1. Advanced Moving Averages

A distinguishing feature of the DAFE strategy is its robust, multi-choice moving averages (MAs). Clients can choose from a wide array of MAs—each with specific strengths—in order to fine-tune their trading signals. The code includes user-defined functions for the following MAs:

imgur.com

Hull Moving Average (HMA):

The hma(src, len) function calculates the HMA by using weighted moving averages (WMAs) to reduce lag considerably while smoothing price data. This function computes an intermediate WMA of half the specified length, then a full-length WMA, and finally applies a further WMA over the square root of the length. This design allows for rapid adaptation to price changes without the typical delays of traditional moving averages.

Triple Exponential Moving Average (TEMA):

Implemented via tema(src, len), TEMA uses three consecutive exponential moving averages (EMAs) to effectively cancel out lag and capture price momentum. The final formula—3 * (ema1 - ema2) + ema3—produces a highly responsive indicator that filters out short-term noise.

Double Exponential Moving Average (DEMA):

Through the dema(src, len) function, DEMA calculates an EMA and then a second EMA on top of it. Its simplified formula of 2 * ema1 - ema2 provides a smoother curve than a single EMA while maintaining enhanced responsiveness.

Volume Weighted Moving Average (VWMA):

With vwma(src, len), this MA accounts for trading volume by weighting the price, thereby offering a more contextual picture of market activity. This is crucial when volume spikes indicate significant moves.

Zero Lag EMA (ZLEMA):

The zlema(src, len) function applies a correction to reduce the inherent lag found in EMAs. By subtracting a calculated lag (based on half the moving average window), ZLEMA is exceptionally attuned to recent price movements.

Arnaud Legoux Moving Average (ALMA):

The alma(src, len, offset, sigma) function introduces ALMA—a type of moving average designed to be less affected by outliers. With parameters for offset and sigma, it allows customization of the degree to which the MA reacts to market noise.

Kaufman Adaptive Moving Average (KAMA):

The custom kama(src, len) function is noteworthy for its adaptive nature. It computes an efficiency ratio by comparing price change against volatility, then dynamically adjusts its smoothing constant. This results in an MA that quickly responds during trending periods while remaining smoothed during consolidation.

Each of these functions—integrated into the strategy—is selectable by the trader (via the fastMAType and slowMAType inputs). This flexibility permits the tailored application of the MA most suited to current market dynamics and individual risk management preferences.

2. ATR-Based Filters and Risk Controls

ATR Calculation and Volatility Filter:

The strategy computes the Average True Range (ATR) over a user-defined period (atrPeriod). ATR is then used to derive both:

Volatility Assessment: Expressed as a ratio of ATR to closing price, ensuring that trades are taken only when volatility remains within a safe, predefined threshold (volatilityThreshold).

ATR-Based Entry Filters: Implemented as atrFilterLong and atrFilterShort, these conditions ensure that for long entries the price is sufficiently above the slow MA and vice versa for shorts. This acts as an additional confirmation filter.

Dynamic Exit Management:

The exit logic employs a dual approach:

Fixed Stop and Profit Target: Stops and targets are set at multiples of ATR (fixedStopMultiplier and profitTargetATRMult), helping manage risk in volatile markets.

Trailing Stop Adjustments: A trailing stop is calculated using the ATR multiplied by a user-defined offset (trailOffset), which captures additional profits as the trade moves favorably while protecting against reversals.

3. Multi-Timeframe Trend Filtering

The strategy enhances its signal reliability by leveraging a secondary, higher timeframe analysis:

15-Minute Trend Analysis:

By retrieving 15-minute moving averages (fastMA15m and slowMA15m) via request.security, the strategy determines the broader market trend. This secondary filter (enabled or disabled through useTrendFilter) ensures that entries are aligned with the prevailing market direction, thereby reducing the incidence of false signals.

4. Signal and Execution Logic

Combined MA Alignment:

The entry conditions are based primarily on the alignment of the fast and slow MAs. A long condition is triggered when the current price is above both MAs and the fast MA is above the slow MA—complemented by the ATR filter and volume conditions. The reverse applies for a short condition.

Volume and Time Window Validation:

Trades are permitted only if the current volume exceeds a minimum (minVolume) and the current hour falls within the predefined trading window (tradingStartHour to tradingEndHour). An additional volume spike check (comparing current volume to a moving average of past volumes) further filters for optimal market conditions.

Comprehensive Order Execution:

The strategy utilizes flexible order execution functions that allow pyramiding (up to 10 positions), ensuring that it can scale into positions as favorable conditions persist. The use of both market entries and automated exits (with profit targets, stop-losses, and trailing stops) ensures that risk is managed at every step.

5. Integrated Dashboard and Metrics

For transparency and real-time analysis, the strategy includes:

On-Chart Visualizations:

Both fast and slow MAs are plotted on the chart, making it easy to see the market’s technical foundation.

Dynamic Metrics Dashboard:

A built-in table displays crucial performance statistics—including current profit/loss, equity, ATR (both raw and as a percentage), and the percentage gap between the moving averages. These metrics offer immediate insight into the health and performance of the strategy.

Input Parameters: Detailed Breakdown

Every input is meticulously designed to offer granular control:

Fast & Slow Lengths:

Determine the window size for the fast and slow moving averages. Smaller values yield more sensitivity, while larger values provide a smoother, delayed response.

Fast/Slow MA Types:

Choose the type of moving average for fast and slow signals. The versatility—from basic SMA and EMA to more complex ones like HMA, TEMA, ZLEMA, ALMA, and KAMA—allows customization to fit different market scenarios.

ATR Parameters:

atrPeriod and atrMultiplier shape the volatility assessment, directly affecting entry filters and risk management through stop-loss and profit target levels.

Trend and Volume Filters:

Inputs such as useTrendFilter, minVolume, and the volume spike condition help confirm that a trade occurs in active, trending markets rather than during periods of low liquidity or market noise.

Trading Hours:

Restricting trade execution to specific hours (tradingStartHour and tradingEndHour) helps avoid illiquid or choppy markets outside of prime trading sessions.

Exit Strategies:

Parameters like trailOffset, profitTargetATRMult, and fixedStopMultiplier provide multiple layers of risk management and profit protection by tailoring how exits are generated relative to current market conditions.

Pyramiding and Fixed Trade Quantity:

The strategy supports multiple entries within a trend (up to 10 positions) and sets a predefined trade quantity (fixedQuantity) to maintain consistent exposure and risk per trade.

Dashboard Controls:

The resetDashboard input allows for on-the-fly resetting of performance metrics, keeping the strategy’s performance dashboard accurate and up-to-date.

Why This Strategy is Truly Exceptional

Multi-Faceted Adaptability:

The ability to switch seamlessly between various moving average types—each suited to particular market conditions—enables the strategy to adapt dynamically. This is a testament to the high level of coding sophistication and market insight infused within the system.

Robust Risk Management:

The integration of ATR-based stops, profit targets, and trailing stops ensures that every trade is executed with well-defined risk parameters. The system is designed to mitigate unexpected market swings while optimizing profit capture.

Comprehensive Market Filtering:

By combining moving average crossovers with volume analysis, volatility thresholds, and multi-timeframe trend filters, the strategy only enters trades under the most favorable conditions. This multi-layered filtering reduces noise and enhances signal quality.

-Final Thoughts-

The Dskyz Adaptive Futures Elite (DAFE) MAtrix with ATR-Powered Precision strategy is not just another trading algorithm—it is a multi-dimensional, fully customizable system built on advanced technical principles and sophisticated risk management techniques. Every function and input parameter has been carefully engineered to provide traders with a system that is both powerful and transparent.

For clients seeking a state-of-the-art trading solution that adapts dynamically to market conditions while maintaining strict discipline in risk management, this strategy truly stands in a class of its own.

****Please show support if you enjoyed this strategy. I'll have more coming out in the near future!!

-Dskyz

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

[SM-042] EMA 5-8-13 with ADX FilterWhat is the strategy?

The strategy combines three exponential moving averages (EMAs) — 5, 8, and 13 periods — with an optional ADX (Average Directional Index) filter. It is designed to enter long or short positions based on EMA crossovers and to exit positions when the price crosses a specific EMA. The ADX filter, if enabled, adds a condition that only allows trades when the ADX value is above a certain threshold, indicating trend strength.

Who is it for?

This strategy is for traders leveraging EMAs and trend strength indicators to make trade decisions. It can be used by anyone looking for a simple trend-following strategy, with the flexibility to adjust for trend strength using the ADX filter.

When is it used?

- **Long trades**: When the 5-period EMA crosses above the 8-period EMA, with an optional ADX condition (if enabled) that requires the ADX value to be above a specified threshold.

- **Short trades**: When the 5-period EMA crosses below the 8-period EMA, with the ADX filter again optional.

- **Exits**: The strategy exits a long position when the price falls below the 13-period EMA and exits a short position when the price rises above the 13-period EMA.

Where is it applied?

This strategy is applied on a chart with any asset on TradingView, with the EMAs and ADX plotted for visual reference. The strategy uses `strategy.entry` to open positions and `strategy.close` to close them based on the set conditions.

Why is it useful?

This strategy helps traders identify trending conditions and filter out potential false signals by using both EMAs (to capture short-term price movements) and the ADX (to confirm the strength of the trend). The ADX filter can be turned off if not desired, making the strategy flexible for both trending and range-bound markets.

How does it work?

- **EMA Crossover**: The strategy enters a long position when the 5-period EMA crosses above the 8-period EMA, and enters a short position when the 5-period EMA crosses below the 8-period EMA.

- **ADX Filter**: If enabled, the strategy checks whether the ADX value is above a set threshold (default is 20) before allowing a trade.

- **Exit Conditions**: Long positions are closed when the price falls below the 13-period EMA, and short positions are closed when the price rises above the 13-period EMA.

- **Plotting**: The strategy plots the three EMAs and the ADX value on the chart for visualization. It also displays a horizontal line at the ADX threshold.

This setup allows for clear decision-making based on the interaction between different time-frame EMAs and trend strength as indicated by ADX.

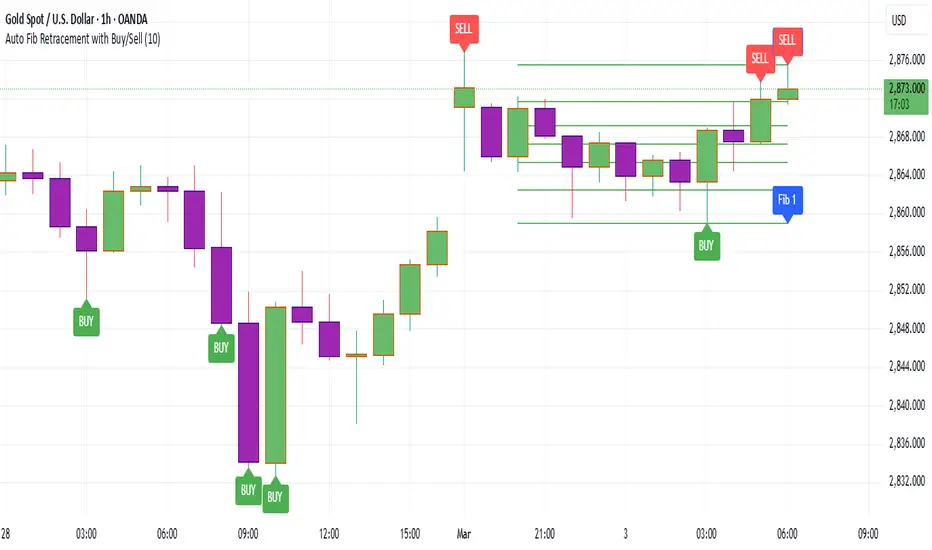

Auto Fib Retracement with Buy/SellKey Features of the Advanced Script:

Multi-Timeframe (MTF) Analysis:

We added an input for the higher timeframe (higher_tf), where the trend is checked on a higher timeframe to confirm the primary trend direction.

Complex Trend Detection:

The trend is determined not only by the current timeframe but also by the trend on the higher timeframe, giving a more comprehensive and reliable signal.

Dynamic Fibonacci Levels:

Fibonacci lines are plotted dynamically, extending them based on price movement, with the Fibonacci retracement drawn only when a trend is identified.

Background Color & Labels:

A background color is added to give a clear indication of the trend direction. Green for uptrend, red for downtrend. It makes it visually easier to understand the current market structure.

"Buy" or "Sell" labels are shown directly on the chart to mark possible entry points.

Strategy and Backtesting:

The script includes strategy commands (strategy.entry and strategy.exit), which allow for backtesting the strategy in TradingView.

Stop loss and take profit conditions are added (loss=100, profit=200), which can be adjusted according to your preferences.

Next Steps:

Test with different timeframes: Try changing the higher_tf to different timeframes (like "60" or "240") and see how it affects the trend detection.

Adjust Fibonacci settings: Modify how the Fibonacci levels are calculated or add more Fibonacci levels like 38.2%, 61.8%, etc.

Optimize Strategy Parameters: Fine-tune the entry/exit logic by adjusting stop loss, take profit, and other strategy parameters.

This should give you a robust foundation for creating advanced trend detection strategies

Strategy SuperTrend SDI WebhookThis Pine Script™ strategy is designed for automated trading in TradingView. It combines the SuperTrend indicator and Smoothed Directional Indicator (SDI) to generate buy and sell signals, with additional risk management features like stop loss, take profit, and trailing stop. The script also includes settings for leverage trading, equity-based position sizing, and webhook integration.

Key Features

1. Date-based Trade Execution

The strategy is active only between the start and end dates set by the user.

times ensures that trades occur only within this predefined time range.

2. Position Sizing and Leverage

Uses leverage trading to adjust position size dynamically based on initial equity.

The user can set leverage (leverage) and percentage of equity (usdprcnt).

The position size is calculated dynamically (initial_capital) based on account performance.

3. Take Profit, Stop Loss, and Trailing Stop

Take Profit (tp): Defines the target profit percentage.

Stop Loss (sl): Defines the maximum allowable loss per trade.

Trailing Stop (tr): Adjusts dynamically based on trade performance to lock in profits.

4. SuperTrend Indicator

SuperTrend (ta.supertrend) is used to determine the market trend.

If the price is above the SuperTrend line, it indicates an uptrend (bullish).

If the price is below the SuperTrend line, it signals a downtrend (bearish).

Plots visual indicators (green/red lines and circles) to show trend changes.

5. Smoothed Directional Indicator (SDI)

SDI helps to identify trend strength and momentum.

It calculates +DI (bullish strength) and -DI (bearish strength).

If +DI is higher than -DI, the market is considered bullish.

If -DI is higher than +DI, the market is considered bearish.

The background color changes based on the SDI signal.

6. Buy & Sell Conditions

Long Entry (Buy) Conditions:

SDI confirms an uptrend (+DI > -DI).

SuperTrend confirms an uptrend (price crosses above the SuperTrend line).

Short Entry (Sell) Conditions:

SDI confirms a downtrend (+DI < -DI).

SuperTrend confirms a downtrend (price crosses below the SuperTrend line).

Optionally, trades can be filtered using crossovers (occrs option).

7. Trade Execution and Exits

Market entries:

Long (strategy.entry("Long")) when conditions match.

Short (strategy.entry("Short")) when bearish conditions are met.

Trade exits:

Uses predefined take profit, stop loss, and trailing stop levels.

Positions are closed if the strategy is out of the valid time range.

Usage

Automated Trading Strategy:

Can be integrated with webhooks for automated execution on supported trading platforms.

Trend-Following Strategy:

Uses SuperTrend & SDI to identify trend direction and strength.

Risk-Managed Leverage Trading:

Supports position sizing, stop losses, and trailing stops.

Backtesting & Optimization:

Can be used for historical performance analysis before deploying live.

Conclusion

This strategy is suitable for traders who want to automate their trading using SuperTrend and SDI indicators. It incorporates risk management tools like stop loss, take profit, and trailing stop, making it adaptable for leverage trading. Traders can customize settings, conduct backtests, and integrate it with webhooks for real-time trade execution. 🚀

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

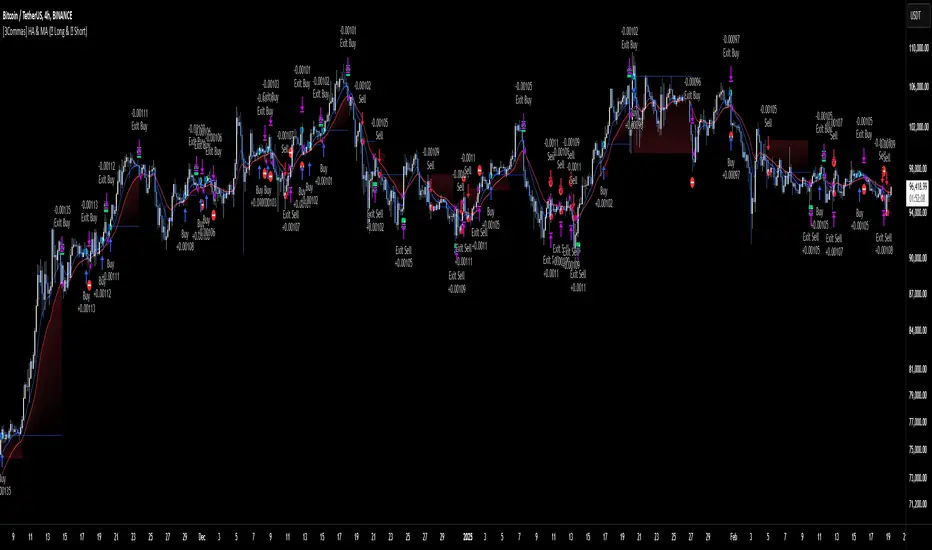

[3Commas] HA & MAHA & MA

🔷What it does: This tool is designed to test a trend-following strategy using Heikin Ashi candles and moving averages. It enters trades after pullbacks, aiming to let profits run once the risk-to-reward ratio reaches 1:1 while securing the position.

🔷Who is it for: It is ideal for traders looking to compare final results using fixed versus dynamic take profits by adjusting parameters and trade direction—a concept applicable to most trading strategies.

🔷How does it work: We use moving averages to define the market trend, then wait for opposite Heikin Ashi candles to form against it. Once these candles reverse in favor of the trend, we enter the trade, using the last swing created by the pullback as the stop loss. By applying the breakeven ratio, we protect the trade and let it run, using the slower moving average as a trailing stop.

A buy signal is generated when:

The previous candle is bearish (ha_bear ), indicating a pullback.

The fast moving average (ma1) is above the slow moving average (ma2), confirming an uptrend.

The current candle is bullish (ha_bull), showing trend continuation.

The Heikin Ashi close is above the fast moving average (ma1), reinforcing the bullish bias.

The real price close is above the open (close > open), ensuring bullish momentum in actual price data.

The signal is confirmed on the closed candle (barstate.isconfirmed) to avoid premature signals.

dir is undefined (na(dir)), preventing repeated signals in the same direction.

A sell signal is generated when:

The previous candle is bullish (ha_bull ), indicating a temporary upward move before a potential reversal.

The fast moving average (ma1) is below the slow moving average (ma2), confirming a downtrend.

The current candle is bearish (ha_bear), showing trend continuation to the downside.

The Heikin Ashi close is below the fast moving average (ma1), reinforcing bearish pressure.

The real price close is below the open (close < open), confirming bearish momentum in actual price data.

The signal is confirmed after the candle closes (barstate.isconfirmed), avoiding premature entries.

dir is undefined (na(dir)), preventing consecutive signals in the same direction.

In simple terms, this setup looks for trend continuation after a pullback, confirming entries with both Heikin Ashi and real price action, supported by moving average alignment to avoid false signals.

If the price reaches a 1:1 risk-to-reward ratio, the stop will be moved to the entry point. However, if the slow moving average surpasses this level, it will become the new exit point, acting as a trailing stop

🔷Why It’s Unique

Easily visualizes the benefits of using risk-to-reward ratios when trading instead of fixed percentages.

Provides a simple and straightforward approach to trading, embracing the "keep it simple" concept.

Offers clear visualization of DCA Bot entry and exit points based on user preferences.

Includes an option to review the message format before sending signals to bots, with compatibility for multi-pair and futures contract pairs.

🔷 Considerations Before Using the Indicator

⚠️Very important: The indicator must be used on charts with real price data, such as Japanese candlesticks, line charts, etc. Do not use it on Heikin Ashi charts, as this may lead to unrealistic results.

🔸Since this is a trend-following strategy, use it on timeframes above 4 hours, where market noise is reduced and trends are clearer. Also, carefully review the statistics before using it, focusing on pairs that tend to have long periods of well-defined trends.

🔸Disadvantages:

False Signals in Ranges: Consolidating markets can generate unreliable signals.

Lagging Indicator: Being based on moving averages, it may react late to sudden price movements.

🔸Advantages:

Trend Focused: Simplifies the identification of trending markets.

Noise Reduction: Uses Heikin Ashi candles to identify trend continuation after pullbacks.

Broad Applicability: Suitable for forex, crypto, stocks, and commodities.

🔸The strategy provides a systematic way to analyze markets but does not guarantee successful outcomes. Use it as an additional tool rather than relying solely on an automated system.

Trading results depend on various factors, including market conditions, trader discipline, and risk management. Past performance does not ensure future success, so always approach the market cautiously.

🔸Risk Management: Define stop-loss levels, position sizes, and profit targets before entering any trade. Be prepared for potential losses and ensure your approach aligns with your overall trading plan.

🔷 STRATEGY PROPERTIES

Symbol: BINANCE:BTCUSDT (Spot).

Timeframe: 4h.

Test Period: All historical data available.

Initial Capital: 10000 USDT.

Order Size per Trade: 1% of Capital, you can use a higher value e.g. 5%, be cautious that the Max Drawdown does not exceed 10%, as it would indicate a very risky trading approach.

Commission: Binance commission 0.1%, adjust according to the exchange being used, lower numbers will generate unrealistic results. By using low values e.g. 5%, it allows us to adapt over time and check the functioning of the strategy.

Slippage: 5 ticks, for pairs with low liquidity or very large orders, this number should be increased as the order may not be filled at the desired level.

Margin for Long and Short Positions: 100%.

Indicator Settings: Default Configuration.

MA1 Length: 9.

MA2 Length: 18.

MA Calculations: EMA.

Take Profit Ratio: Disable. Ratio 1:4.

Breakeven Ratio: Enable, Ratio 1:1.

Strategy: Long & Short.

🔷 STRATEGY RESULTS

⚠️Remember, past results do not guarantee future performance.

Net Profit: +324.88 USDT (+3.25%).

Max Drawdown: -81.18 USDT (-0.78%).

Total Closed Trades: 672.

Percent Profitable: 35.57%.

Profit Factor: 1.347.

Average Trade: +0.48 USDT (+0.48%).

Average # Bars in Trades: 13.

🔷 HOW TO USE

🔸 Adjust Settings:

The default values—MA1 (9) and MA2 (18) with EMA calculation—generally work well. However, you can increase these values, such as 20 and 40, to better identify stronger trends.

🔸 Choose a Symbol that Typically Trends:

Select an asset that tends to form clear trends. Keep in mind that the Strategy Tester results may show poor performance for certain assets, making them less suitable for sending signals to bots.

🔸 Experiment with Ratios:

Test different take profit and breakeven ratios to compare various scenarios—especially to observe how the strategy performs when only the trade is protected.

🔸This is an example of how protecting the trade works: once the price moves in favor of the position with a 1:1 risk-to-reward ratio, the stop loss is moved to the entry price. If the Slow MA surpasses this level, it will act as a trailing stop, aiming to follow the trend and maximize potential gains.

🔸In contrast, in this example, for the same trade, if we set a take profit at a 1:3 risk-to-reward ratio—which is generally considered a good risk-reward relationship—we can see how a significant portion of the upward move is left on the table.

🔸Results Review:

It is important to check the Max Drawdown. This value should ideally not exceed 10% of your capital. Consider adjusting the trade size to ensure this threshold is not surpassed.

Remember to include the correct values for commission and slippage according to the symbol and exchange where you are conducting the tests. Otherwise, the results will not be realistic.

If you are satisfied with the results, you may consider automating your trades. However, it is strongly recommended to use a small amount of capital or a demo account to test proper execution before committing real funds.

🔸Create alerts to trigger the DCA Bot:

Verify Messages: Ensure the message matches the one specified by the DCA Bot.

Multi-Pair Configuration: For multi-pair setups, enable the option to add the symbol in the correct format.

Signal Settings: Enable whether you want to receive long or short signals (Entry | TP | SL), copy and paste the the messages for the DCA Bots configured.

Alert Setup:

When creating an alert, set the condition to the indicator and choose "alert() function call only.

Enter any desired Alert Name.

Open the Notifications tab, enable Webhook URL, and paste the Webhook URL.

For more details, refer to the section: "How to use TradingView Custom Signals".

Finalize Alerts: Click Create, you're done! Alerts will now be sent automatically in the correct format.

🔷 INDICATOR SETTINGS

MA 1: Fast MA Length

MA 2: Slow MA Length

MA Calc: MA's Calculations (SMA,EMA, RMA,WMA)

TP Ratio: This is the take profit ratio relative to the stop loss, where the trade will be closed in profit.

BE Ratio: This is the breakeven ratio relative to the stop loss, where the stop loss will be updated to breakeven or if the MA2 is greater than this level.

Strategy: Order Type direction in which trades are executed.

Use Custom Test Period: When enabled signals only works in the selected time window. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

Check Messages: Enable the table to review the messages to be sent to the bot.

Entry | TP | SL: Enable this options to send Buy Entry, Take Profit (TP), and Stop Loss (SL) signals.

Deal Entry and Deal Exit : Copy and paste the message for the deal start signal and close order at Market Price of the DCA Bot. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the bot so that it can process properly so that it executes and starts the trade.

DCA Bot Multi-Pair: You must activate it if you want to use the signals in a DCA Bot Multi-pair in the text box you must enter (using the correct format) the symbol in which you are creating the alert, you can check the format of each symbol when you create the bot.

👨🏻💻💭 We hope this tool helps enhance your trading. Your feedback is invaluable, so feel free to share any suggestions for improvements or new features you'd like to see implemented.

__

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

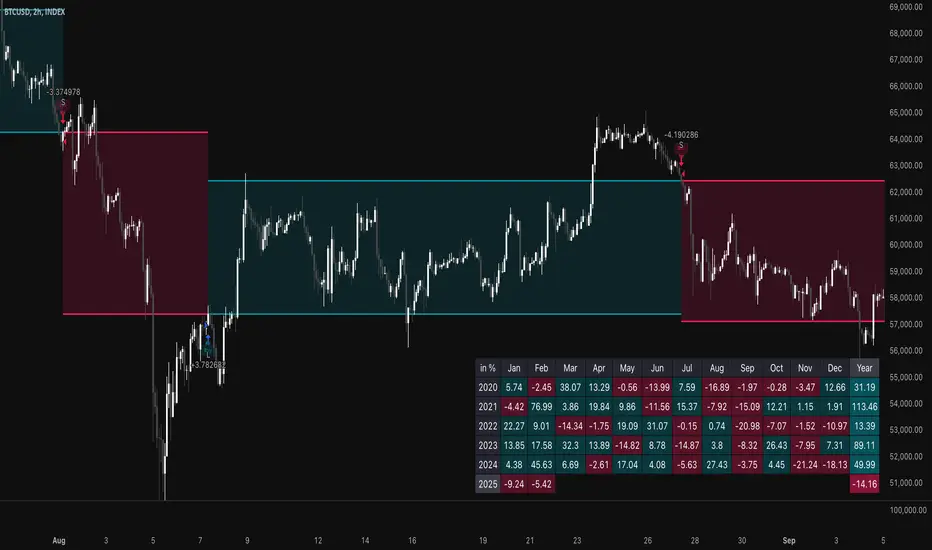

TSI Long/Short for BTC 2HThe TSI Long/Short for BTC 2H strategy is an advanced trend-following system designed specifically for trading Bitcoin (BTC) on a 2-hour timeframe. It leverages the True Strength Index (TSI) to identify momentum shifts and executes both long and short trades in response to dynamic market conditions.

Unlike traditional moving average-based strategies, this script uses a double-smoothed momentum calculation, enhancing signal accuracy and reducing noise. It incorporates automated position sizing, customizable leverage, and real-time performance tracking, ensuring a structured and adaptable trading approach.

🔹 What Makes This Strategy Unique?

Unlike simple crossover strategies or generic trend-following approaches, this system utilizes a customized True Strength Index (TSI) methodology that dynamically adjusts to market conditions.

🔸 True Strength Index (TSI) Filtering – The script refines the TSI by applying double exponential smoothing, filtering out weak signals and capturing high-confidence momentum shifts.

🔸 Adaptive Entry & Exit Logic – Instead of fixed thresholds, it compares the TSI value against a dynamically determined high/low range from the past 100 bars to confirm trade signals.

🔸 Leverage & Risk Optimization – Position sizing is dynamically adjusted based on account equity and leverage settings, ensuring controlled risk exposure.

🔸 Performance Monitoring System – A built-in performance tracking table allows traders to evaluate monthly and yearly results directly on the chart.

📊 Core Strategy Components

1️⃣ Momentum-Based Trade Execution

The strategy generates long and short trade signals based on the following conditions:

✅ Long Entry Condition – A buy signal is triggered when the TSI crosses above its 100-bar highest value (previously set), confirming bullish momentum.

✅ Short Entry Condition – A sell signal is generated when the TSI crosses below its 100-bar lowest value (previously set), indicating bearish pressure.

Each trade execution is fully automated, reducing emotional decision-making and improving trading discipline.

2️⃣ Position Sizing & Leverage Control

Risk management is a key focus of this strategy:

🔹 Dynamic Position Sizing – The script calculates position size based on:

Account Equity – Ensuring trade sizes adjust dynamically with capital fluctuations.

Leverage Multiplier – Allows traders to customize risk exposure via an adjustable leverage setting.

🔹 No Fixed Stop-Loss – The strategy relies on reversals to exit trades, meaning each position is closed when the opposite signal appears.

This design ensures maximum capital efficiency while adapting to market conditions in real time.

3️⃣ Performance Visualization & Tracking

Understanding historical performance is crucial for refining strategies. The script includes:

📌 Real-Time Trade Markers – Buy and sell signals are visually displayed on the chart for easy reference.

📌 Performance Metrics Table – Tracks monthly and yearly returns in percentage form, helping traders assess profitability over time.

📌 Trade History Visualization – Completed trades are displayed with color-coded boxes (green for long trades, red for short trades), visually representing profit/loss dynamics.

📢 Why Use This Strategy?

✔ Advanced Momentum Detection – Uses a double-smoothed TSI for more accurate trend signals.

✔ Fully Automated Trading – Removes emotional bias and enforces discipline.

✔ Customizable Risk Management – Adjust leverage and position sizing to suit your risk profile.

✔ Comprehensive Performance Tracking – Integrated reporting system provides clear insights into past trades.

This strategy is ideal for Bitcoin traders looking for a structured, high-probability system that adapts to both bullish and bearish trends on the 2-hour timeframe.

📌 How to Use: Simply add the script to your 2H BTC chart, configure your leverage settings, and let the system handle trade execution and tracking! 🚀

00 Averaging Down Backtest Strategy by RPAlawyer v21FOR EDUCATIONAL PURPOSES ONLY! THE CODE IS NOT YET FULLY DEVELOPED, BUT IT CAN PROVIDE INTERESTING DATA AND INSIGHTS IN ITS CURRENT STATE.

This strategy is an 'averaging down' backtester strategy. The goal of averaging/doubling down is to buy more of an asset at a lower price to reduce your average entry price.

This backtester code proves why you shouldn't do averaging down, but the code can be developed (and will be developed) further, and there might be settings even in its current form that prove that averaging down can be done effectively.

Different averaging down strategies exist:

- Linear/Fixed Amount: buy $1000 every time price drops 5%

- Grid Trading: Placing orders at price levels, often with increasing size, like $1000 at -5%, $2000 at -10%

- Martingale: doubling the position size with each new entry

- Reverse Martingale: decreasing position size as price falls: $4000, then $2000, then $1000

- Percentage-Based: position size based on % of remaining capital, like 10% of available funds at each level

- Dynamic/Adaptive: larger entries during high volatility, smaller during low

- Logarithmic: position sizes increase logarithmically as price drops

Unlike the above average costing strategies, it applies averaging down (I use DCA as a synonym) at a very strong trend reversal. So not at a certain predetermined percentage negative PNL % but at a trend reversal signaled by an indicator - hence it most closely resembles a dynamically moving grid DCA strategy.

Both entering the trade and averaging down assume a strong trend. The signals for trend detection are provided by an indicator that I published under the name '00 Parabolic SAR Trend Following Signals by RPAlawyer', but any indicator that generates numeric signals of 1 and -1 for buy and sell signals can be used.

The indicator must be connected to the strategy: in the strategy settings under 'External Source' you need to select '00 Parabolic SAR Trend Following Signals by RPAlawyer: Connector'. From this point, the strategy detects when the indicator generates buy and sell signals.

The strategy considers a strong trend when a buy signal appears above a very conservative ATR band, or a sell signal below the ATR band. The conservative ATR is chosen to filter ranging markets. This very conservative ATR setting has a default multiplier of 8 and length of 40. The multiplier can be increased up to 10, but there will be very few buy and sell signals at that level and DCA requirements will be very high. Trade entry and DCA occur at these strong trends. In the settings, the 'ATR Filter' setting determines the entry condition (e.g., ATR Filter multiplier of 9), and the 'DCA ATR' determines when DCA will happen (e.g., DCA ATR multiplier of 6).

The DCA levels and DCA amounts are determined as follows:

The first DCA occurs below the DCA Base Deviation% level (see settings, default 3%) which acts as a threshold. The thick green line indicates the long position avg price, and the thin red line below the green line indicates the 3% DCA threshold for long positions. The thick red line indicates the short position avg price, and the thin red line above the thick red line indicates the short position 3% DCA threshold. DCA size multiplier defines the DCA amount invested.

If the loss exceeds 3% AND a buy signal arrives below the lower ATR band for longs, or a sell signal arrives above the upper ATR band for shorts, then the first DCA will be executed. So the first DCA won't happen at 3%, rather 3% is a threshold where the additional condition is that the price must close above or below the ATR band (let's say the first DCA occured at 8%) – this is why the code resembles a dynamic grid strategy, where the grid moves such that alongside the first 3% threshold, a strong trend must also appear for DCA. At this point, the thick green/red line moves because the avg price is modified as a result of the DCA, and the thin red line indicating the next DCA level also moves. The next DCA level is determined by the first DCA level, meaning modified avg price plus an additional +8% + (3% * the Step Scale Multiplier in the settings). This next DCA level will be indicated by the modified thin red line, and the price must break through this level and again break through the ATR band for the second DCA to occur.

Since all this wasn't complicated enough, and I was always obsessed by the idea that when we're sitting in an underwater position for days, doing DCA and waiting for the price to correct, we can actually enter a short position on the other side, on which we can realize profit (if the broker allows taking hedge positions, Binance allows this in Europe).

This opposite position in this strategy can open from the point AFTER THE FIRST DCA OF THE BASE POSITION OCCURS. This base position first DCA actually indicates that the price has already moved against us significantly so time to earn some money on the other side. Breaking through the ATR band is also a condition for entry here, so the hedge position entry is not automatic, and the condition for further DCA is breaking through the DCA Base Deviation (default 3%) and breaking through the ATR band. So for the 'hedge' or rather opposite position, the entry and further DCA conditions are the same as for the base position. The hedge position avg price is indicated by a thick black line and the Next Hedge DCA Level is indicated by a thin black line.

The TPs are indicated by green labels for base positions and red labels for hedge positions.

No SL built into the strategy at this point but you are free to do your coding.

Summary data can be found in the upper right corner.

The fantastic trend reversal indicator Machine learning: Lorentzian Classification by jdehorty can be used as an external indicator, choose 'backtest stream' for the external source. The ATR Band multiplicators need to be reduced to 5-6 when using Lorentz.

The code can be further developed in several aspects, and as I write this, I already have a few ideas 😊

Z-Strike RecoveryThis strategy utilizes the Z-Score of daily changes in the VIX (Volatility Index) to identify moments of extreme market panic and initiate long entries. Scientific research highlights that extreme volatility levels often signal oversold markets, providing opportunities for mean-reversion strategies.

How the Strategy Works

Calculation of Daily VIX Changes:

The difference between today’s and yesterday’s VIX closing prices is calculated.

Z-Score Calculation:

The Z-Score quantifies how far the current change deviates from the mean (average), expressed in standard deviations:

Z-Score=(Daily VIX Change)−MeanStandard Deviation

Z-Score=Standard Deviation(Daily VIX Change)−Mean

The mean and standard deviation are computed over a rolling period of 16 days (default).

Entry Condition:

A long entry is triggered when the Z-Score exceeds a threshold of 1.3 (adjustable).

A high positive Z-Score indicates a strong overreaction in the market (panic).

Exit Condition:

The position is closed after 10 periods (days), regardless of market behavior.

Visualizations:

The Z-Score is plotted to make extreme values visible.

Horizontal threshold lines mark entry signals.

Bars with entry signals are highlighted with a blue background.

This strategy is particularly suitable for mean-reverting markets, such as the S&P 500.

Scientific Background

Volatility and Market Behavior:

Studies like Whaley (2000) demonstrate that the VIX, known as the "fear gauge," is highly correlated with market panic phases. A spike in the VIX is often interpreted as an oversold signal due to excessive hedging by investors.

Source: Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Z-Score in Financial Strategies:

The Z-Score is a proven method for detecting statistical outliers and is widely used in mean-reversion strategies.

Source: Chan, E. (2009). Quantitative Trading. Wiley Finance.

Mean-Reversion Approach:

The strategy builds on the mean-reversion principle, which assumes that extreme market movements tend to revert to the mean over time.

Source: Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

MultiLayer Acceleration/Deceleration Strategy [Skyrexio]Overview

MultiLayer Acceleration/Deceleration Strategy leverages the combination of Acceleration/Deceleration Indicator(AC), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Acceleration/Deceleration Indicator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Acceleration/Deceleration shall create one of two types of long signals (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created long signal.

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one long signal, another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. We'll begin with the simplest: the EMA.

The Exponential Moving Average (EMA) is a type of moving average that assigns greater weight to recent price data, making it more responsive to current market changes compared to the Simple Moving Average (SMA). This tool is widely used in technical analysis to identify trends and generate buy or sell signals. The EMA is calculated as follows:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy, the EMA acts as a long-term trend filter. For instance, long trades are considered only when the price closes above the EMA (default: 100-period). This increases the likelihood of entering trades aligned with the prevailing trend.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

In this strategy if the most recent up fractal breakout occurs above the Alligator's teeth and follows the last down fractal breakout below the teeth, the algorithm identifies an uptrend. Long trades can be opened during this phase if a signal aligns. If the price breaks a down fractal below the teeth line during an uptrend, the strategy assumes the uptrend has ended and closes all open long trades.

By combining the EMA as a long-term trend filter with the Alligator and fractals as short-term filters, this approach increases the likelihood of opening profitable trades while staying aligned with market dynamics.

Now let's talk about Acceleration/Deceleration signals. AC indicator is calculated using the Awesome Oscillator, so let's first of all briefly explain what is Awesome Oscillator and how it can be calculated. The Awesome Oscillator (AO), developed by Bill Williams, is a momentum indicator designed to measure market momentum by contrasting recent price movements with a longer-term historical perspective. It helps traders detect potential trend reversals and assess the strength of ongoing trends.

The formula for AO is as follows:

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

The Acceleration/Deceleration (AC) Indicator, introduced by Bill Williams, measures the rate of change in market momentum. It highlights shifts in the driving force of price movements and helps traders spot early signs of trend changes. The AC Indicator is particularly useful for identifying whether the current momentum is accelerating or decelerating, which can indicate potential reversals or continuations. For AC calculation we shall use the AO calculated above is the following formula:

AC = AO − SMA5(AO), where SMA5(AO)is the 5-period Simple Moving Average of the Awesome Oscillator

When the AC is above the zero line and rising, it suggests accelerating upward momentum.

When the AC is below the zero line and falling, it indicates accelerating downward momentum.

When the AC is below zero line and rising it suggests the decelerating the downtrend momentum. When AC is above the zero line and falling, it suggests the decelerating the uptrend momentum.

Now we can explain which AC signal types are used in this strategy. The first type of long signal is when AC value is below zero line. In this cases we need to see three rising bars on the histogram in a row after the falling one. The second type of signals occurs above the zero line. There we need only two rising AC bars in a row after the falling one to create the signal. The signal bar is the last green bar in this sequence. The strategy places the buy stop order one tick above the candle's high, which corresponds to the signal bar on AC indicator.

After that we can have the following scenarios:

Price hit the order on the next candle in this case strategy opened long with this price.

Price doesn't hit the order price, the next candle set lower high. If current AC bar is increasing buy stop order changes by the script to the high of this new bar plus one tick. This procedure repeats until price finally hit buy order or current AC bar become decreasing. In the second case buy order cancelled and strategy wait for the next AC signal.

If long trades are initiated, the strategy continues utilizing subsequent signals until the total number of trades reaches a maximum of 5. All open trades are closed when the trend shifts to a downtrend, as determined by the combination of the Alligator and Fractals described earlier.

Why we use AC signals? If currently strategy algorithm considers the high probability of the short-term uptrend with the Alligator and Fractals combination pointed out above and the long-term trend is also suggested by the EMA filter as bullish. Rising AC bars after period of falling AC bars indicates the high probability of local pull back end and there is a high chance to open long trade in the direction of the most likely main uptrend. The numbers of rising bars are different for the different AC values (below or above zero line). This is needed because if AC below zero line the local downtrend is likely to be stronger and needs more rising bars to confirm that it has been changed than if AC is above zero.

Why strategy use only 10% per signal? Sometimes we can see the false signals which appears on sideways. Not risking that much script use only 10% per signal. If the first long trade has been open and price continue going up and our trend approximation by Alligator and Fractals is uptrend, strategy add another one 10% of capital to every next AC signal while number of active trades no more than 5. This capital allocation allows to take part in long trades when current uptrend is likely to be strong and use only 10% of capital when there is a high probability of sideways.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.11.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 10%

Maximum Single Position Loss: -5.15%

Maximum Single Profit: +24.57%

Net Profit: +2108.85 USDT (+21.09%)

Total Trades: 111 (36.94% win rate)

Profit Factor: 2.391

Maximum Accumulated Loss: 367.61 USDT (-2.97%)

Average Profit per Trade: 19.00 USDT (+1.78%)

Average Trade Duration: 75 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 3h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

MultiLayer Awesome Oscillator Saucer Strategy [Skyrexio]Overview

MultiLayer Awesome Oscillator Saucer Strategy leverages the combination of Awesome Oscillator (AO), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Awesome Oscillator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Awesome Oscillator shall create the "Saucer" long signal (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created "Saucer signal".

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one "Saucer" signal another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's go through all concepts used in this strategy to understand how they works together. Let's start from the easies one, the EMA. Let's briefly explain what is EMA. The Exponential Moving Average (EMA) is a type of moving average that gives more weight to recent prices, making it more responsive to current price changes compared to the Simple Moving Average (SMA). It is commonly used in technical analysis to identify trends and generate buy or sell signals. It can be calculated with the following steps:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy uses EMA an initial long term trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

Let's go to the next, short-term trend filter which consists of Alligator and Fractals. Let's briefly explain what do these indicators means. The Williams Alligator, developed by Bill Williams, is a technical indicator designed to spot trends and potential market reversals. It uses three smoothed moving averages, referred to as the jaw, teeth, and lips:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When these lines diverge and are properly aligned, the "alligator" is considered "awake," signaling a strong trend. Conversely, when the lines overlap or intertwine, the "alligator" is "asleep," indicating a range-bound or sideways market. This indicator assists traders in identifying when to act on or avoid trades.

The Williams Fractals, another tool introduced by Bill Williams, are used to pinpoint potential reversal points on a price chart. A fractal forms when there are at least five consecutive bars, with the middle bar displaying the highest high (for an up fractal) or the lowest low (for a down fractal), relative to the two bars on either side.

Key Points:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often combine fractals with other indicators to confirm trends or reversals, improving the accuracy of trading decisions.

How we use their combination in this strategy? Let’s consider an uptrend example. A breakout above an up fractal can be interpreted as a bullish signal, indicating a high likelihood that an uptrend is beginning. Here's the reasoning: an up fractal represents a potential shift in market behavior. When the fractal forms, it reflects a pullback caused by traders selling, creating a temporary high. However, if the price manages to return to that fractal’s high and break through it, it suggests the market has "changed its mind" and a bullish trend is likely emerging.

The moment of the breakout marks the potential transition to an uptrend. It’s crucial to note that this breakout must occur above the Alligator's teeth line. If it happens below, the breakout isn’t valid, and the downtrend may still persist. The same logic applies inversely for down fractals in a downtrend scenario.

So, if last up fractal breakout was higher, than Alligator's teeth and it happened after last down fractal breakdown below teeth, algorithm considered current trend as an uptrend. During this uptrend long trades can be opened if signal was flashed. If during the uptrend price breaks down the down fractal below teeth line, strategy considered that uptrend is finished with the high probability and strategy closes all current long trades. This combination is used as a short term trend filter increasing the probability of opening profitable long trades in addition to EMA filter, described above.

Now let's talk about Awesome Oscillator's "Sauser" signals. Briefly explain what is the Awesome Oscillator. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

Now we know what is AO, but what is the "Saucer" signal? This concept was introduced by Bill Williams, let's briefly explain it and how it's used by this strategy. Initially, this type of signal is a combination of the following AO bars: we need 3 bars in a row, the first one shall be higher than the second, the third bar also shall be higher, than second. All three bars shall be above the zero line of AO. The price bar, which corresponds to third "saucer's" bar is our signal bar. Strategy places buy stop order one tick above the price bar which corresponds to signal bar.